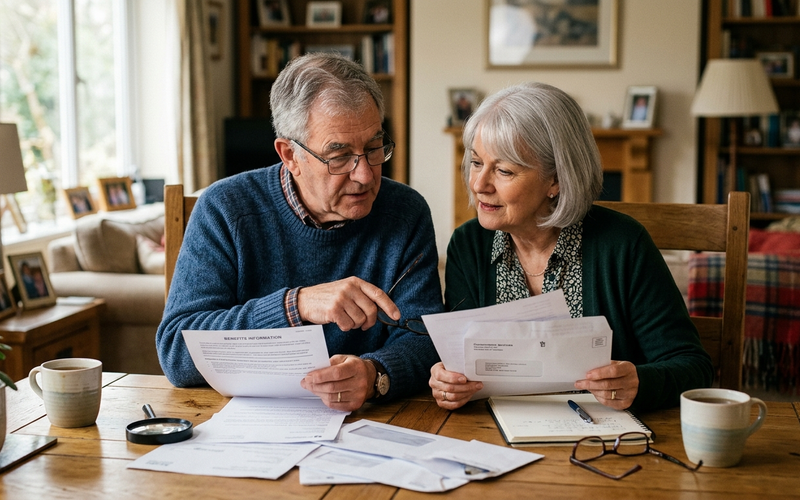

How to Protect Your Aging Parents: Must-Have Legal Checklist & Documents

Did you know that 68% of Americans don’t have a will? This startling statistic reveals how unprepared many of us are when it comes to protecting our aging parents legally. Unfortunately, this lack of preparation can have serious consequences. If your elderly loved one needs Medicaid, missing financial documents could delay or even prevent approval…

Sixty-eight percent of Americans don't have a will. For many families, this means no legal plan is in place if an aging parent becomes incapacitated or dies.

Without proper documents, problems pile up quickly. A missing financial document can delay or block Medicaid approval. Without military records, a veteran's benefits go unclaimed. When a medical crisis hits and there's no living will, no one knows what the patient actually wants.

That's why a legal checklist matters. A durable power of attorney keeps working even if your parent can't make decisions. A healthcare proxy lets someone you trust make medical calls when your parent can't. These documents prevent the court from stepping in and making choices your parent would have hated.

This guide covers what documents you need, how to get them, and where to keep them. Whether you're starting from scratch or updating old paperwork, you'll find a checklist that helps ensure your aging parents get the protection they need.

- Start with the basics: core legal documents for aging parents

- Build a safety net: financial and identity documents

Organizing your parent's financial and identity documents protects them from fraud and makes it easier to handle their affairs if they get sick or need care. Bank statements, insurance policies, property deeds—when these are in one place and accessible, your family won't scramble in a crisis. - Secure and store: how to organize and access documents

- Conclusion

- FAQs

Start with the basics: core legal documents for aging parents

Legal documents do one thing: they preserve your parent's wishes and keep their affairs running even if they can't make decisions anymore.

A durable power of attorney for finances is the first one to get. This names someone to handle money decisions if your parent becomes unable to do it. A regular power of attorney expires if the person gets incapacitated. A durable one doesn't.

A healthcare power of attorney (also called a healthcare proxy) does the same thing for medical decisions. If your parent can't talk to doctors or make choices about treatment, the person you name can do it for them.

A living will (or advance healthcare directive) tells doctors what your parent wants if they're dying—CPR or no CPR, feeding tubes or not, comfort care. It's the instruction manual for the hardest decisions.

A last will and testament says who gets what after death. Many elder law attorneys also suggest a revocable living trust, which lets your parent stay in control of assets during life and passes them smoothly to beneficiaries after.

Without these documents, the court steps in. Judges decide who gets guardianship or conservatorship. They might make choices that contradict what your parent wanted, and they'll take a cut of the estate for court fees.

Talk to an elder law attorney to make sure these documents fit your state's rules and actually say what your parent needs them to say.

Build a safety net: financial and identity documents

About 23% of adult children worry about managing their aging parents' finances and estates. Good reason—it's complicated without organized records.

Start by listing income: Social Security, pensions, investments. List all bank accounts and retirement accounts (401(k)s, IRAs, annuities). Write down what they're worth and who to contact.

Insurance matters: life, health, long-term care, home, auto. Get policy numbers and agent contact info. You'll need these for claims and healthcare decisions.

Property documents: deeds to houses, titles to cars, mortgage paperwork. These get needed if you sell or transfer ownership.

For proof of identity, gather birth certificates, marriage/divorce papers, driver's license, passport, Social Security card, and military ID. Hospitals and senior communities ask for these constantly.

Tax returns: Keep at least seven years' worth, along with W-2s and 1099 forms. The IRS only requires three, but seven covers edge cases.

Access matters. Joint ownership of accounts works when the owner dies, unlike a power of attorney that ends at death. But each bank has different rules, so ask.

Put it all in one system—digital with strong encryption or physical with good organization. When Medicaid or VA benefits get denied because paperwork's missing, you'll wish you had.

Secure and store: how to organize and access documents

Having documents doesn't help if you can't find them in an emergency. A good storage system is half the battle.

Keep originals in a fireproof, waterproof safe—wills, powers of attorney, deeds. A safety deposit box works too, but banks sometimes freeze access when the account holder dies, so keep copies elsewhere. Give at least one trusted family member a key or password and the location.

Digital copies save time. No more hunting through filing cabinets. You can scan documents with a scanner or phone camera, organize them on a computer, and access from anywhere. Here's how:

- Gather all documents

- Scan them (use a scanner or camera app)

- Name and organize files clearly

- Store securely

Security matters. Use encrypted cloud storage (Google Drive, Dropbox, iCloud) or an encrypted external hard drive. Make passwords long (at least 12 characters) with uppercase, lowercase, numbers, and symbols. Turn on two-factor authentication. Install antivirus software.

Build an emergency binder: clearly labeled sections for different document types, kept someplace secure but easy to reach. When crisis hits, your family knows exactly where to look.

Update it. After a password change, new document, health change, or major life event, review and refresh. This takes 15 minutes and prevents outdated information from causing problems.

Conclusion

Preparing documents for an aging parent is practical care. Durable powers of attorney, healthcare proxies, and living wills prevent confusion when medical emergencies hit. They respect what your parent actually wants instead of leaving it to strangers.

Financial documents matter too. Organized bank accounts, investments, insurance policies, and property records let the family manage things smoothly if circumstances change. Without them, people get lost in paperwork during an already difficult time.

How you store these documents determines whether they're useful. A fireproof safe for originals, encrypted digital copies for access, a binder in the kitchen for emergencies—the method matters less than reliability. Set it up now, and your family won't be scrambling later.

Families that do this work handle healthcare, banks, and legal systems faster and with fewer mistakes. It feels overwhelming at first, but breaking it into steps makes it doable. This is how you honor what your parents want and protect their security in their later years.

FAQs

Q1. What are the essential legal documents for aging parents? Durable power of attorney for finances, healthcare power of attorney, living will or advance healthcare directive, last will and testament, and sometimes a revocable living trust. These protect your parent's wishes and interests.

Q2. How can I safeguard my elderly parents' financial and identity information?

List all financial accounts, insurance policies, property deeds, and identity documents. Include bank statements, investment details, tax returns, birth certificates, and Social Security cards. Store securely and tell at least one trusted family member where everything is.

Q3. What's the best way to store and organize important documents for aging parents? Use both physical and digital storage. Keep originals in a fireproof safe or safety deposit box. Scan documents and store copies on encrypted cloud storage or a hard drive. Organize everything with clear labels and an emergency binder. Make sure at least one family member knows the locations and passwords.

Q4. How often should I update my parents' legal and financial documents? Review them annually and after major changes: health problems, financial shifts, or significant life events. This ensures they still match your parents' actual situation.

Q5. What steps can I take to protect my elderly parents' assets?

Create an estate plan with durable power of attorney and healthcare power of attorney. This lets you manage assets and make medical decisions if needed. Watch for fraud and scams targeting older adults. Set up account alerts and consider limiting access to accounts.

Get matched

Looking for senior care for someone you love?

Tell us what you're considering. We'll share independent matches and pricing directly with you. No phone calls until you ask for one.

- Takes about two minutes to complete.

- Pricing details emailed to you. No phone calls until you ask for one.

- Independent matching. We do not own the communities we list.

Loading the matching form…

Powered by SilverAssist. By submitting this form you agree to our privacy policy.

More from our editors

All articles

Medicare's First Negotiated Drug Prices Are Now in Effect for 2026

For the first time, Medicare negotiated the price of 10 top prescription drugs, and those lower prices took effect on January 1, 2026. Here are the 10 drugs, how far the prices dropped, whether you will actually pay less at the pharmacy, and the 15 more drugs, including Ozempic and Wegovy, that follow in 2027.

Medicare Now Covers Weight-Loss GLP-1 Drugs at $50 a Month

On July 1, 2026, Medicare launched a demonstration program that lets eligible Part D enrollees fill Wegovy, Foundayo, or Zepbound for $50 a month - the first time the program has covered drugs used solely for weight loss. Who qualifies, what the $50 copay does not cover, and what to ask your doctor.

Senior Benefits in 2026: What Changed, What's Coming, and What's Just a Proposal

Higher Medicare premiums, a new Part D cap, tougher SNAP rules, an earlier Social Security shortfall: 2026 brought real changes to senior benefits, plus big proposals still moving through Congress. Here is a plain-language rundown of what is law now and what is not.

Explore senior living options

Comparing care for yourself or a family member? Browse communities by care type and see what each option typically costs.

- Assisted livingHelp with daily activities, costs, and how to choose a community.

- Independent livingMaintenance-free communities for active older adults.

- Home careIn-home support for seniors aging in place.

- Nursing homesSkilled nursing care and Medicare star ratings.

- Senior apartmentsAge-restricted, budget-friendly rental housing.

- Cost of senior livingCompare typical monthly prices by care type and state.